Daniel Elias

Daniel Elias

Marketing, Jibrel

One of the most exciting possibilities afforded by decentralized networks is the ability to build a decentralized financial world.

DeFi (Decentralized Finance) envisions a future in which all traditional banking services can be offered through a decentralized network and enforced using smart contracts. It would enable consumers to borrow and repay money autonomously, allow investors to buy asset-backed securities and see transactions made securely whilst adhering to the proper regulations.

While institutional grade custody is a fundamental building block required to achieve this, the ability to tokenize different assets is the other side of the coin. A $10 trillion security token market is unfolding, combining the power of blockchain technology with standardized securities.

What Does Tokenization Achieve?

Crypto assets have largely been thought of as currencies for much of their existence, in no small part owing to the original intention of Bitcoin. However, as the space has progresses, the aims of crypto assets have expanded.

Rather than holding a market based and often abstract value, tokenization enables tokens to be backed by assets such as precious metals. real estate or company equity. This, therefore, provides them with an intrinsic value while providing a number of improvements for investors and consumers alike such as:

- Fractional ownership & liquidity of hard to split assets such as commercial real estate and fine art continue to be characterized by low liquidity high unit costs.

- 24/7 markets that go way beyond the stock market’s typical, 9:30 a.m. — 4:00 p.m. (EST), typical business hours. Tokenized assets would be traded in the same fashion as BTC or ETH.

- Rapid settlement has the potential to increase settlement speed for securities, settling transactions in minutes versus days.

- Costs reduction in administrative, middle/back office, and compliance may be greatly reduced due to automation. These include activities such as distributions, redemptions and proxy voting, which can be programmed via smart contracts to improve efficiency.

Tokenization doesn’t need to subvert the entire investment process; it merely aims to streamline it by removing intermediaries and reducing costs.

An example of this comes with regulatory burdens such as KYC and AML which can be programmed in at the network level. A business can make it such that their tokenized real estate can only be transferred to previously KYC/AML approved individuals residing in specific countries.

Investor identity would be linked to a crypto asset wallet. If an investor tries to trade the tokens to a non-approved individual, the transaction will fail. This removes the need for each party to perform due diligence on each investor and makes it such that it only has to be performed once.

Although tokenization does not guarantee liquidity, it does provide investors with access to targeted opportunities that would otherwise have been out of reach. This might include, for example, the ability purchase equity in the form of tokens in a specific building.

Taking it to an extreme, this could lead asset owners to bundle together assets in a manner that wasn’t previously possible, benefiting from increased access to capital. Although this will need to take place within existing regulatory guidelines, securely backed tokens could encourage global investors to invest in previously localized opportunities.

What is the Current Landscape?

Tokenization is far from a finished product. There remains problems in how to ensure a token is truly backed by the asset it purports to be, as well as issues in ensuring the enforcement of this.

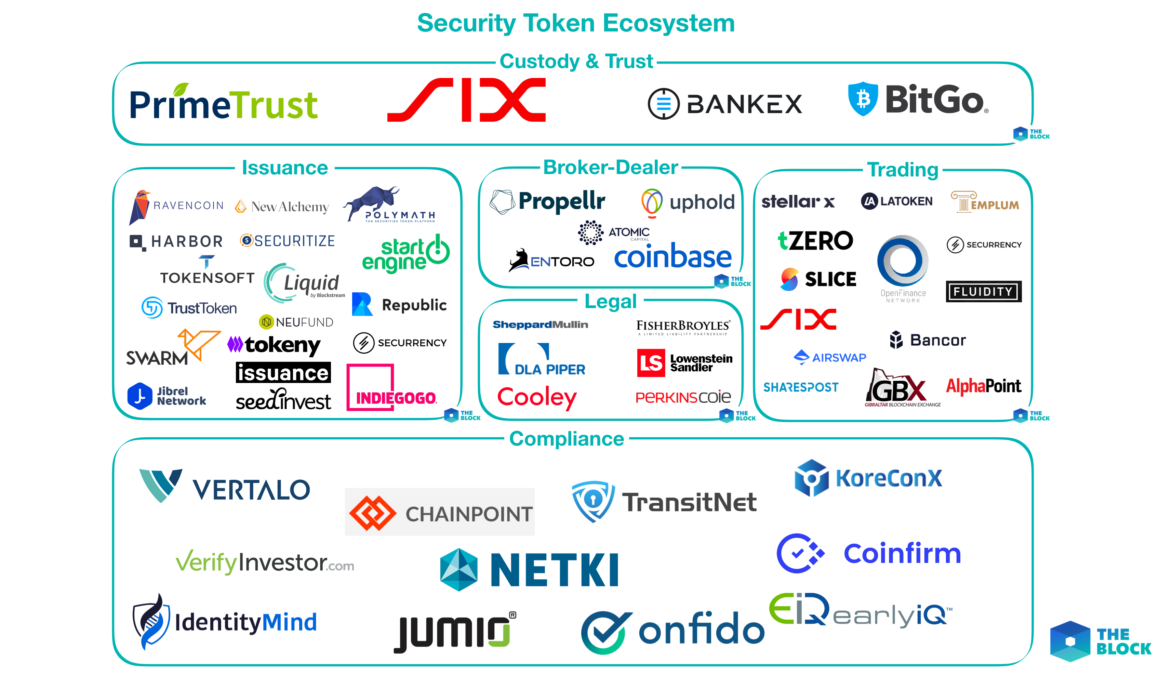

Regulations on crypto assets, in general, are unclear across many jurisdictions, and they are no more precise on this subset. While tokenization remains in its infancy, there is a growing swell of parties involved in the space.

The Security Token Ecosystem (The Block)

The Security Token Ecosystem (The Block)

These companies are currently building much of the infrastructure required for tokenized assets.

While there are further services which will need to be created, including market data services and research/ratings that are common to traditional markets, but the foundations are being formed.

According to a report by PWC, 28 Security Token Offerings (STOs) raised $442 million in 2018, with 2019–20 expected to see that figure increase dramatically.

One such STO, tZERO (the subsidiary of e-Commerce giant Overstock), is a good example of how tokenized assets can work in practice.

Over 1,000 investors worldwide contributed to the initial $134 million STO raise, with the tokens they purchased able to be held either by a broker or in their own personal wallets. These tokens will then be freely tradeable once the tZERO platform launches in 2019.

The company itself aims to build a trading platform specifically designed for tokenized assets, and has signed a deal with a private equity firm to enable the trading of rare minerals such as cobalt on the platform.

While much of the focus has been on issuance and trading, arguably the most important aspect to enable investors to partake in DeFi is custodial solutions.

The Swiss stock exchange SIX is developing a trading platform for tokenized assets, known as SIX Digital Exchange. This will come under the same Swiss financial regulations as the core exchange and will be a “fully integrated trading, settlement, and custody infrastructure” for digital assets which is intended to expand to include assets like fine art.

Most crypto asset custodial options to date have been launched by crypto first companies, such as Coinbase or Xapo. It should not be a surprise that custodial solutions for tokenized assets are being launched by existing financial service companies, given their regulatory knowledge and the close relationship to traditional assets.

Another Swiss entity, the investment bank Vontobel, launched the Digital Asset Vault to provide trading and custodial solutions to banks and asset managers. Vontobel’s offering again ties in with the existing regulations they already adhere to with normal assets.

As tokenization becomes more popular in the coming years, the number of interested parties is likely to swell dramatically, both from crypto first companies and existing financial institutions.

Jibrel’s Vision

The ability to tokenize real-world assets and bring them ‘on-chain’ is a key part of Jibrel’s vision. There are various different types of such assets that need to be tokenized, including:

- Currencies and commodities (for value storage and transfer)

- Debt instruments (for automated lending)

- Securitized debt instruments (for trading)

Jcash is a representation of this, providing currency backed digital tokens (such as EUR, USD, GBP, and KRW). These ‘crypto-fiats’are fully backed by their underlying assets, meaning consumers can be confident their assets are guaranteed in the event that Jibrel ceases to exist or operate.

However, fiat currencies are just the first of many different types of assets that will be brought on-chain.

Jibrel was the first company to execute a Sukuk transaction on a blockchain, using Ethereum to enable the Al Hilal Bank to sell part of the Islamic bond issuance.

This issuance exemplified many of the efficiency gains issuers can expect, including facilitating clearing and settlement, reduced settlement risk exposure, lower transaction costs and a network that is functioning and available at all times.

Jibrel also partnered with the SEED Group, through which it aims to tokenize US$250 million of their financial assets.

In the next 12 months, Jibrel will have added to Jcash and pilots such as the above by enabling the use and transactions of commodities, real-estate and Sukuk/bonds over Ethereum. This will enable a much wider range of asset-owners to tokenize their assets and will open up opportunities that previously did not exist.

In addition to making token issuance possible, there is also a requirement to provide institutional grade storage and transaction solutions.

This includes wallets, with the Jwallet intended to provide bank level security while maintaining full user control. It enables users to search through transactions and balances in a manner with which banking customers and institutional investors have grown familiar.

Future iterations will also facilitate detailed analytics of transfers and balances, as well as allow regulated transactions, including KYC/AML checks on blockchain addresses. These are critical functionalities that seasoned investors will require if they are to adopt digital assets.

If institutional investors are expected to adopt tokenized securities, providing such solutions is a key step. There is little point facilitating a tokenized world if there are limited investor-ready digital asset solutions.

While most crypto wallets that currently exist primarily focus on enabling users to send and receive crypto-currencies, the Jwallet has been designed from the ground-up to facilitate the usage of crypto-assets.

Daniel Elias, Marketing at Jibrel

Daniel Elias, Marketing at Jibrel

Daniel is on the Jibrel marketing team, a blockchain company that provides currencies, equities, commodities and other financial assets as standard ERC-20 tokens on the Ethereum blockchain. He is a growth hacker with a background in management consulting that has helped banks such as JP Morgan, Goldman Sachs and HSBC with digital transformation before making the transition to startups.