Did you end up taking a loss in crypto markets in 2018? If the answer was yes, here’s some good news: the IRS will let you write off some or perhaps even all of that loss. Crypto loss deductions reduce your taxable income, thus saving you a significant amount of money at tax time.

Even if you only held onto your crypto assets and didn’t sell at all, it’s still important to report your cryptocurrency holdings anyway. Read on to find out why.

![]()

The Myth of Cryptocurrency Anonymity

If you use Coinbase, Kraken, Gemini or any other of the major cryptocurrency exchanges in the US, you likely had to submit identifying documents when you registered. This means that if the IRS were to investigate you, it could theoretically connect your name to all your crypto assets. That’s why it’s important to account for your crypto holdings each year at tax time. If you don’t, your omission could come back to haunt you later.

Though anonymous cryptocurrencies like Monero and DASH do exist, most cryptos are only semi-anonymous.

The reason: crypto transactions are recorded to publicly accessible ledgers. Whoever knows your address can find out how much money you have. Unless you’ve been extremely careful to safeguard your cryptocurrency data, you’re holdings are not nearly as private as you may believe.

The Good News About Crypto Taxes

If you earned profits in crypto markets last year, you’ll have to add that income to the other income that you received in 2018. However, if you lost money you can file a capital loss. All you have to do is determine exactly how much you lost and then use that information to fill out IRS form 8949.

In addition, HOLDers (crypto investors that hold onto their crypto assets in the hopes that prices will eventually skyrocket) may not have much tax exposure. The reason: the IRS only considers a capital gain or loss to be realized at the time of sale.

Generate Your Tax Report Today by Using CoinTracking.info

The quickest and easiest way to learn how much you owe the IRS– or how big of a deduction you can get– is with CoinTracking.info. CoinTracking.info was one of the very first crypto tax calculators to hit the market. Since 2014, CoinTracking.info’s developers have been adding features and refining its interface. Over 300,000 people trust CoinTracking.info and many of them are CPAs.

CPA Laura Walter has produced a series of video courses that are designed to help her clients learn how to get the most out of CoinTracking.info. Watch the video below to learn how to get started.

Step 1: Connect Your Exchanges

CoinTracking.info is one of the few crypto tax calculators that supports API integration. API integration makes it easy to quickly and easy import data from your crypto exchanges with a minimum of hassle.

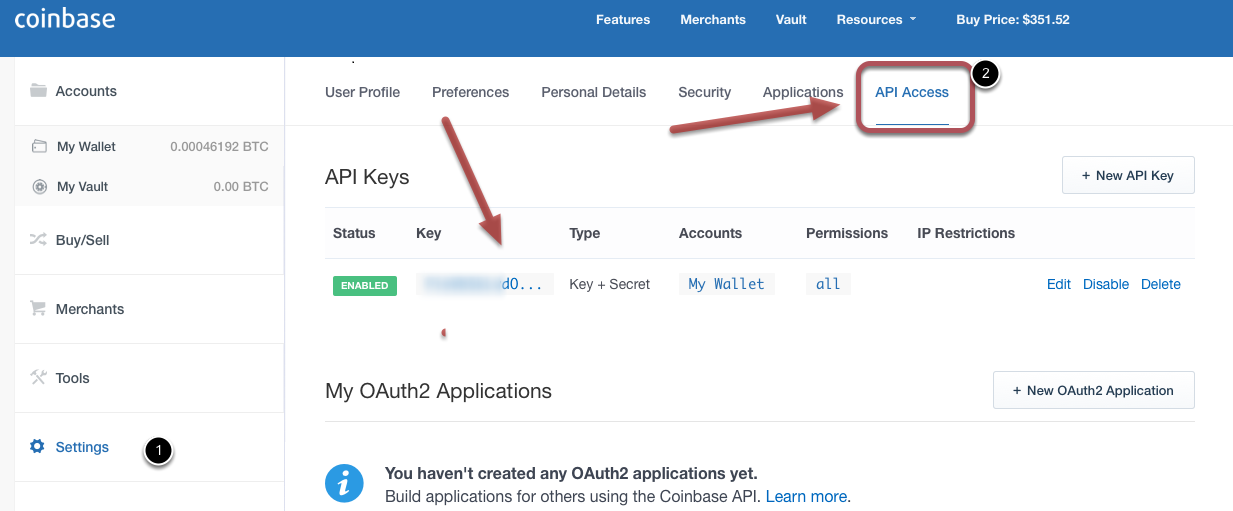

If you use Coinbase, for example, all you have to do is click API Access from the settings menu and then select New API Key. Then, just copy and paste your API key into CoinTracking.info. The process is virtually the same on all other exchanges that have accessible APIs.

Step 2: Import Your Wallet Data

After you’ve imported your exchange account information, the next step in getting started is importing your wallet data. You should report all your crypto holdings, even your long term positions. Forgetting to report your long term holdings will create a hard-to-solve tax problem for you in the future.

CoinTracking.info supports all the most popular Bitcoin wallets, from Blockchain.info to Trezor.

Step 3: Reconcile Your Deposits and Withdrawals

Did you use any of your exchange accounts to deposit crypto payments or transfer mining revenues? If the answer was yes– and you forgot to make a note when you made each of these transactions– you should reconcile all your deposits and withdrawals.

Fortunately, this is very easy to do with CoinTracking.info. After you import all your transactions, you can export them to a spreadsheet and use filters to identify all the transactions you need to label. CPA Laura Walter explains how to do this in the video embedded above.

Step 4: Check Your Work

Before you export your tax report, you should go back and check your work to make sure that your information makes sense. An easy way to do this is with CoinTracking.info’s “Balance by Exchange” chart. This chart lets you make sure that all your cryptocurrency balances are positive.

If you see any negative values, that’s a sign that you may need to check again to see if there are any outstanding transactions that require reconciliation.

Summary

Doing your crypto taxes isn’t as complicated as you might assume. With CoinTracking.info, you can generate a very accurate tax report in 20 minutes or less. The software automatically generates all the cost basis information you need to learn how much you gained or lost during the year.

Once you have this information, all you have to do is submit IRS form 8949. CoinTracking.info automatically generates this form for you and fills it in with all the information you need to submit. Get a free CoinTracking.info account and generate your tax report today.